Joule Assets Part I: How to Draw Investors to Energy Efficiency

Energy efficiency and money seem like the stuff of a Zen riddle. The energy efficiency market is worth at least $900 billion.* But try to find financing for a project and no money exists.

For investors it’s a problem of scale. Most building retrofit projects are too small to create attractive returns for investors.

“A critical issue for investors is that there is nothing to securitize. There is no solid revenue flow for these projects,” said Mike Gordon, CEO of Joule Assets, in a recent interview

However, gather many energy efficiency projects together into a portfolio and suddenly they look golden.

That’s the premise underlying Joule Assets strategy to bring to the energy efficiency industry the secret sauce that made solar so big: financing that works for smaller projects.

In a recent interview, Gordon explained how Joule Assets finances small to medium projects through its new $100 million fund and what kind of investment it seeks.

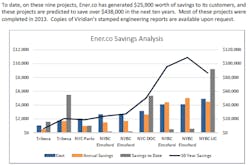

The New York company recently announced its first deal, the financing of $1 million in projects by Ener.co, a company that offers a nanotechnology, spray-on coating that increases the energy performance of HVAC systems. Ener.co treats equipment in a range of building types: multi-family residential, industrial, hospitals, universities, prisons and others

In this kind of deal, the contractor acts as aggregator, and the investor is spared the need to conduct due diligence on hundreds or even thousands of energy efficiency projects to bring the deal to scale. The contractor provides security on 20 percent of the cash flow and takes the first hit if any failure occurs. So one in five projects might fail, and the investor remains whole. This puts the onus on the contractor to carefully choose which deals it brings into the aggregation.

“The contractor gets the benefit of a line of credit that is five times what appears on their balance sheet. But they are the first loss,” Gordon said. “So when they are in a room looking to close a deal, they have to make a judgment whether that counterparty is good.”

In Ener.co’s case, the company is able to spread risk among a wide range of projects and pieces of equipment, said Carlos Cervantes, Ener.co’s chief strategic officer. “Not every piece of equipment we treat will have the same return profile,” he said. This allows Ener.co to take on a riskier piece of equipment, since that risk is offset by measures that guarantee energy savings. “It is not just rolling up customers, it is rolling up energy conservation measures within a portfolio,” he said.

Seeking missing cash flow

But Joule Assets looks for more than that. It seeks products with additional cash flow potential that the contractor has missed. “There is value in these projects that these contractors have no idea about,” Gordon said.

He described three potential sources of cash flow, beyond the foundational requirements, that Joule Assets has identified. These are:

- Active cash flow: Specific value streams (eg. energy efficiency credits, forward capacity market payments) that the contractor hasn’t incorporated into the project. Joule Assets helps the contractor register for those streams.

- Activist cash flow: No current value stream exists, but may if a state government, an agency, legislature or utility takes certain actions. It may require new legislation or market changes.

- Building future value: Joule Assets engages strategically in the contractor’s future and receives warrants in its equity. For example, in the case of Ener.co, there are several ways Joule Assets can increase the company’s future value. This might include connecting the company with a larger number of customers. It might involve registering the peak demand reduction achieved by Ener.co with the grid operator and writing an algorithm that makes every future project Ener.co does more valuable. Or Joule Assets might help Ener.co document the kilowatt-hours it saves to help build a rebate program with a state agency or utility. Joule Assets would build this value in exchange for warrants in the company

In Part II of this story, Gordon talks about the investment prospects for microgrids. Watch for us to post the story on EnergyEfficiencyMarkets.com, or subscribe to our free newsletter so that it is delivered directly to your mailbox.

*McKinsey Global Institute, The Case for Investing in Energy Productivity

About the Author

Elisa Wood

Editor-in-Chief

Elisa Wood is the editor and founder of EnergyChangemakers.com. She is co-founder and former editor of Microgrid Knowledge.