Switching Gears: The U.S. Move Toward Gas-Insulated MV Switchgear

- Traditionally, air-insulated electrical switchgear dominated the market due to cost-effectiveness and widespread commercial availability.

- Market trends are evolving as new sectors require more compact, reliable, and technologically advanced switchgear solutions.

- It's not just about adapting but staying ahead of these trends will be essential for companies looking to remain competitive in this rapidly changing landscape.

The US medium-voltage (MV) electric switchgear market is radically shifting mainly due to increased electricity demand, technological advancements, and sector-specific developments. Traditionally, air-insulated electrical switchgear (AIS) dominated the market due to cost-effectiveness and widespread commercial availability. However, with the evolution of the overall market landscape, a noticeable shift toward advanced solutions such as gas-insulated switchgear (GIS) is being observed specifically in high-growth sectors like data centers and renewable energy.

This article provides an overview of the MV switchgear market in the US, including a discussion on drivers of demand in the market. It also explores the latest trends in switchgear technology and the expansion of manufacturing capacity by original equipment manufacturers (OEMs) in the US switchgear market.

Overview of the MV GIS Market in the US

According to PTR estimates, the MV GIS market within the data center segment is expected to experience substantial growth, with a projected compound annual growth rate (CAGR) of 16% from 2023 to 2030. This growth rate is nearly double the overall industry CAGR for GIS, indicating significant investment and expansion opportunities in this market segment.

In contrast, the renewable energy (RE) sector is predicted to grow steadily, with PTR forecasting a CAGR of 12% in revenue during the same period. This highlights the diverse dynamics and growth potential across these key sectors within the MV switchgear market.

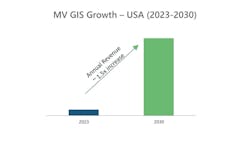

Additionally, annual revenue in the U.S. MV GIS market is expected to increase by approximately 1.5 times during the same timeframe, further underscoring the sector’s upward trajectory.

Drivers of the MV GIS market in the U.S.

The U.S. MV GIS market is driven by exponential growth in data centers and the widespread adoption of renewable energy in the country.

Exponential growth of data centers

The rapid expansion of data centers nationwide is driving the demand in the MV GIS market. The exponential growth of data centers is driven by advancements in generative artificial intelligence (AI) and increasing dependence on cloud computing, which necessitate highly reliable and efficient power systems.

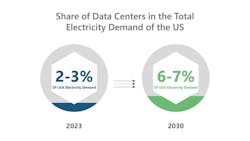

According to PTR estimates in 2023, data centers accounted for 2-3% of the total electricity consumption, however, by 2030, the data centers are expected to account for nearly 6% of the total electricity consumption in the US, with peak demand doubling due to increasing rack densities.

The existing facilities are transitioning from LV to MV GIS to effectively manage high current requirements. The shift is driven by the need to optimize space and improve the reliability of power distribution in environments with drastically increasing energy demands.

For hyperscale facilities, the trend is towards implementing state-of-the-art electricity network topologies, enabling the incorporation of multiple GIS units. These advanced topologies can support high power demands and redundancy requirements of large-scale data centers, in turn improving reliability and ensuring cost-effectiveness while complying with T4 tier classification standards.

Widespread adoption of renewable energy

The United States is leading the global transition toward renewable energy with the introduction of ambitious clean energy targets and supportive policy frameworks. The US has set an aggressive clean energy target to develop 30 GW of offshore wind farms, followed by an average installation of 60 GW of solar capacity from 2025 onwards till 2030.

These goals are widely supported by major investments through the Inflation Reduction Act (IRA) and the Infrastructure Investment and Jobs Act (IIJA), which collectively allocated USD 446 billion for the clean energy sector. The massive influx of investment has led to a surge in renewable energy projects, with the interconnection queue for renewable generation and storage projects reaching 2,600 GW in 2023. PTR expects that demand for MV GIS in the country will be triggered as these projects come online.

Trends in the Switchgear Technology

In North America, the medium-voltage (MV) switchgear market has been predominantly dominated by air-insulated switchgear (AIS), with 2023-unit volumes outpacing gas-insulated switchgear (GIS) by nearly a 6:1 ratio. AIS has been favored due to its cost-effectiveness and straightforward installation, making it the preferred choice for numerous applications, as mentioned earlier.

However, market trends are evolving as new sectors require more compact, reliable, and technologically advanced switchgear solutions. Gas-insulated switchgear (GIS) is increasingly preferred, especially in applications where space is limited, and higher reliability is essential.

There has also been a shift towards SF6-free switchgear in the global market. Europe is leading the transition with plans to ban SF6-based MV switchgear by 2032; the US is also following suit. Leading OEMs are phasing out SF6 across their operations, including in the US. This shift represents a notable change from the historical predominance of AIS and signals a broader trend towards a sustainable power grid in the US.

PG&E, a utility in the US, has proactively adopted SF6-free switchgear and phased out SF6-based switchgear at medium voltage levels. The utility is also aiming to avoid utilizing SF6 in all high voltage gas insulated equipment.

Manufacturing Expansion in the US

OEMs are pushing to expand their manufacturing capabilities to cater to the country's increasing demand for electric switchgear. For instance, Siemens has committed USD 150 million to build a new manufacturing facility in the Dallas-Fort Worth area to meet the demand from data centers and critical infrastructure. On the other hand, Siemens is investing USD 54 million in enhancing existing Texas and California facilities.

To increase the output of circuit breakers and associated electrical equipment for customers in North America, Schneider Electric is modernizing operations and investing in manufacturing plants in Lexington, Kentucky, Lincoln, and Nebraska.

OEMs are also moving to expand their product portfolios. Siemens, with the introduction of 8DAB 40 switchgear, which utilizes clean air as an insulating medium and is free from harmful fluorinated gases, has broadened sustainable blue GIS offerings.

Similarly, Schneider Electric has announced plans to invest $140 million in its U.S. manufacturing operations, in 2024. The investment includes $85 million to upgrade facilities in Mt. Juliet and Smyrna, Tennessee, to produce electrical switchgear and medium voltage power distribution products for infrastructure and data center demand.

Such expansions are indicative of the industry's awareness of the rising demand for sustainable switchgear solutions, specifically gas-insulated switchgear.

Looking Ahead

The U.S. MV switchgear market is at a pivotal moment, with significant growth on the horizon driven by the expansion of data centers and the rise of renewable energy projects. As the market continues to evolve, industry stakeholders must adapt to these changes by investing in new technologies, expanding manufacturing capacities, and addressing supply chain challenges.

However, it's not just about adapting but staying ahead of these trends will be essential for companies looking to remain competitive in this rapidly changing landscape.

About the Author

Muhammad Usman

Muhammad Usman

Analyst - PTR Inc.

Muhammad Usman is an Analyst at Power Grid at PTR, specializing in MV and HV switchgear market analysis. He is passionate about an SF6-free future and digitalization in the energy sector and works closely with clients to provide effective solutions. He has a Master's degree in Energy Systems Engineering and has contributed to market reforms in Pakistan's electricity sector through a USAID project.

About PTR: With over a decade of experience in the Power Grid and New Energy sector, PTR Inc. has evolved from a core market research firm into a comprehensive Strategic Growth Partner, empowering clients’ transitions and growth in the renewable energy landscape and E-mobility, particularly within the electrical infrastructure manufacturing space.