Behind-the-Meter Energy Storage Breaks Records in Q2: GTM Research

Behind-the-meter energy storage hit record highs in the United States for the second quarter, according to numbers published today by GTM Research and the Energy Storage Association.

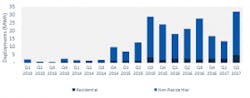

During the second quarter, 443 residential and commercial energy systems were deployed, representing 32 MWh of capacity.

Looking at the big picture, the Q3 2017 U.S. Energy Storage Monitor showed a total 50.4 MWh of energy storage deployed in the second quarter. This is up 6 percent year-over-year.

U.S. Behind-the-Meter Energy Storage Deployments by Segment

Source: GTM Research/ESA U.S. Energy Storage Monitor, Q3 2017

What pushed this record-breaking quarter? According to the report, much of the growth, especially in the residential sector, came from new products in California and Hawaii connecting to the grid. For example, 71 percent of Hawaii’s second-quarter activity came from the Customer Self-Supply program, which saw a slight rise in activity last quarter after “several quarters of sluggishness.”

[clickToTweet tweet=”In Q2, 443 residential and commercial energy systems were deployed across the United States. #behindthegrid'” quote=”In Q2, 443 residential and commercial energy systems were deployed across the United States. #behindthegrid”]

Brett Simon, an energy storage analyst at GTM Research and one of the report’s authors, gave more color on residential sector movement, with a special focus on action in the Golden State.

“California held the lead in behind-the-meter deployments as the Self-Generation Incentive Program (SGIP) queue continues to clear,” said Simon. “Toward the end of this year, we expect to see more SGIP-related deployment activity as the first deployments from the modified program, which opened in May, start to be interconnected. Furthermore, we expect to see greater growth from California’s residential segment in the next few years given the residential carve-out under the latest version of SGIP and changes to TOU rates for solar customers.”

California & NY lead non-residential market

California saw the most deployments for the non-residential segment with 12,030 kW.

California also leads the non-residential market for deployments with 12,030 kW, followed by New York with 1,300 kW. Massachusetts rounded out the top three for the second quarter with 250 kW deployed.

The total non-residential market, which includes commercial, industrial, religious, military, and non-profit behind-the-meter deployments, rose to 27.3 MWh in the second quarter. This represents impressive growth of 151 percent over the first quarter this year.

But there’s a bit of a roadblock for New York’s growth in this area, Simon explained.

“New York experienced an uptick in non-residential deployments this quarter, though challenges around lithium-ion system permitting in New York City have slowed the market despite a massive opportunity identified by developers,” he said.

Lastly, the front-of-meter segment, which is normally the largest group of deployments, saw the tides turn a bit this past quarter. The segment dropped down to 18.5 MWh deployed in Q2 after enjoying two consecutive prior quarters of more than 200 MWh newly deployed.

This downward movement may be explained in part by recent projects coming to completion in California. According to the report, most of the Aliso Canyon projects came on-line in prior quarters, which boosted deployment numbers above the norm.

But the news wasn’t all bad for the front-of-meter segment. Several states, including Arizona, Nevada, New Jersey, New Mexico and Virginia introduced or made progress on “policies and proceedings that work to encourage utilities to accommodate storage in distribution planning and renewable integration efforts,” the report stated.

U.S.-based investors dominate

It seems U.S.-based investors are stepping up to the plate to fund these new storage deployments.

According to GTM Research’s comparison of investment from U.S.-based versus European-based investors, total dollars committed to storage have been higher from U.S.-based entities. Last year, $275 million was invested in storage from U.S.-based investors, which represents about four times the $94 million storage from European-based firms.

U.S. Energy Storage Deployments, 2012-2022E

Source: GTM Research/ESA U.S. Energy Storage Monitor, Q3 2017

GTM Research also pointed out that U.S.-based organizations continue to become increasingly interested in storage, and are coming back to the pool to invest larger amounts.

For example, the largest deal from a U.S.-based investor in 2016 was $200 million (CIT Bank project financing for Advanced Microgrid Solutions). And for a European-based investor that number was $85M (eCapital’s investment in Sonnen).

Energy storage to reach 2.5 GW by 2022

All the interest, movement and growth in the U.S. energy storage market is further illustrated in GTM Research’s predictions for future deployments.

The firm asserts the U.S. energy storage market will grow to roughly 2.5 GW in 2022, which is 11 times the size of the 2016 market of 231 MW.

Breaking the numbers down further, the behind-the-meter segment represented 19 percent of the 2016 storage market. GTM Research predicts this will grow to 26 percent in 2017 and 52 percent by 2022.

California is expected to remain atop the heap for new storage deployments over the next five years, with Arizona, Hawaii, Massachusetts, New York and Texas battling it out for second place.

What’s driving this expected growth? According to GTM, momentum is “driven by a combination of state mandates, resource-planning-related utility procurement, and the increasingly favorable economics of behind-the-meter storage projects.”

$3.1 billion market in the U.S. by 2022

Looking at this growth in dollars, by 2022, the U.S. energy storage market is expected to be worth $3.1 billion, according to the report – nine times bigger than the 2016 market. This growth will likely push revenues in 2017 to grow by 43 percent over 2016.

“Cumulative 2017-2022 storage market revenues will be $10.4 billion,” GTM reported.

The utility segment, which accounted for $252 million and 76 percent of the market last year, is expected to continue to be the largest segment through 2022, although the residential segment alone is predicted to represent a $1.2 billion market by that time.

Looking forward to the rest of the year, GTM Research doesn’t expect growth to slow for the overall energy storage market. The company predicts 591 MWh of storage to be deployed across all segments by the end of 2017.

Track news about behind-the-meter energy storage. Subscribe to the Microgrid Knowledge newsletter. It’s free.