The New Incentive Landscape: What Microgrid Developers Need to Know About BABA and FEOC Restrictions

Key Highlights

- The One Big Beautiful Bill Act has significantly reduced and tightened federal funding options for renewable energy projects, introducing new eligibility criteria.

- BABA mandates sourcing construction and certain manufactured materials domestically, with specific thresholds for component costs, impacting project procurement strategies.

- FEOC restrictions now prohibit foreign entities from participating in projects claiming key tax credits, with expanded definitions and new categories like SFEs and FIEs.

- Projects must now meet Material Assistance Cost Ratio (MACR) thresholds, which increase annually, to qualify for tax credits, emphasizing the importance of sourcing non-FEOC materials.

- Expert guidance, such as from ELM MicroGrid, is crucial for navigating these complex regulations, ensuring compliance, and maximizing project incentives.

Noah Bowman

PUBLIC POLICY ANALYST

ELM Microgrid

In an increasingly volatile and ever-shifting policy landscape for energy projects, especially renewables and energy storage, owners and operators face increasingly stringent regulations regarding projects’ eligibility for federal funds and incentives. As a result of the One Big Beautiful Bill Act (OBBBA), many long-time incentives for renewable energy projects, namely the Section 48E Clean Energy Investment Tax Credit (ITC), are being eliminated through accelerated phaseouts. There are, however, several incentives still available, particularly for battery storage systems.

Understanding the new criteria to claim these credits is essential to locking in long-term project funding, but unpacking the differences in scope, applicability, and requirements of these regulations can be complex, especially since they often overlap and interact within the same project. Compliance with one requirement does not necessarily mean compliance with another; each has their own conditions of eligibility and their own timeline, and each also carries its own level of stringency regarding their tolerance for the involvement of non-domestic materials or project components.

Most prominent among these restrictions are the Foreign Entity of Concern (FEOC) rules, a series of regulations on the involvement of foreign governments and entities from specific countries, namely Russia, China, North Korea, and Iran, that prohibit and/or limit their involvement in projects seeking to claim certain tax credits, including the Clean Energy ITC. These restrictions have existed since the Inflation Reduction Act of 2022, but the OBBBA has expanded the FEOC definition and created more specific categories of classification: Specified Foreign Entities (SFEs) and Foreign-Influenced Entities (FIEs). For the purposes of FEOC regulations, both types of entities are considered Prohibited Foreign Entities (PFEs).

Specified Foreign Entities consist of a specific list of entities and firms barred from receiving federal incentives, including Chinese military companies operating in the U.S., firms otherwise associated with the Chinese military, entities subject to the Uyghur Forced Labor Prevention Act (UFLPA), battery producing entities deemed ineligible for U.S. Department of Defense contracts, and foreign-controlled entities.

A Foreign Influenced Entity, meanwhile, is an entity that a Specified Foreign Entity exerts influence on, meeting any of the following criteria:

· An SFE can directly or indirectly appoint a board or executive officer

· An SFE holds 25% or greater ownership

· An SFE owns an aggregated 40% or more alongside other SFEs

· An SFE holds an aggregated 15% of the debt or more

· The entity made a payment to an SFE that allows them to exercise “effective control” over a qualified facility, energy storage, technology, or eligible component.

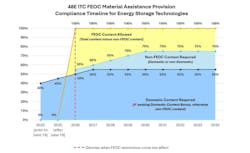

Under these new FEOC restrictions, any of the above PFEs are prohibited from directly claiming many federal tax credits, including the Clean Energy ITC, effective immediately. Additionally, any project seeking these tax credits must prove it is not receiving “significant material assistance” from a PFE by meeting a specified Material Assistance Cost Ratio (MACR) threshold. The MACR is essentially the percentage amount of the project component cost which is not sourced from PFEs. The MACR threshold varies based on whether a project is considered wind/solar generation or energy storage technology for the purposes of the ITC. Beginning in 2026, the MACR threshold for wind and solar projects is 40%, and for energy storage, it is 55%. This means that for a project beginning construction in 2026 to be eligible to receive the ITC, 40% or more of their project cost must be derived from non-FEOC-sourced materials. This threshold then increases by five percent each year; since wind and solar projects generally aren’t eligible for the ITC if they begin construction after 2027, their MACR threshold caps at 45%. For energy storage projects, however, ITC availability extends through 2030; thus, the MACR threshold will continue to increase every year before reaching a cap of 75% in 2030.

The Domestic Content Bonus Adder for the Clean Energy ITC is a similar provision, though it functions as a carrot instead of a stick. The Domestic Content Bonus provides an additional 10% increase to the base 30% ITC credit if a minimum percentage of the project’s component cost is sourced from the U.S. (along with 100% of the steel and/or iron content of the project, with some exceptions). It’s important to note that while meeting the requirements of this bonus is optional, it is stricter than the FEOC provision. FEOC compliance can be achieved with internationally sourced components so long as PFEs are avoided; domestic content compliance, as the name suggests, must be met with components from the U.S. Like the MACR threshold under FEOC rules, the minimum required Domestic Content percentage to claim the adder has increased annually; for projects that begin construction in 2026, the required domestic content percentage is 50%. For projects beginning construction in 2027, the required percentage reaches its cap of 55%. Additionally, projects above 1 MW must meet the prevailing wage and apprenticeship requirements outlined in the IRA, else the domestic content bonus will only add two additional percentage points (2%) to the 30% ITC credit.

As the incentive landscape continues to narrow for renewable generation while remaining open—though more complex—for energy storage, success will increasingly depend on early, deliberate compliance planning. FEOC eligibility, MACR thresholds, and Domestic Content requirements each impose distinct and escalating constraints that cannot be evaluated in isolation. Project owners and operators that proactively map supply chains, ownership structures, and procurement strategies against these evolving rules will be best positioned to preserve ITC eligibility, maximize available adders, and protect long-term project economics in an increasingly constrained federal incentive environment.

Sponsored by: