Carbon Emissions Fell Again in the U.S. Northeast. So What’s the Next Step for RGGI?

Carbon emissions fell again in 2016 for the U.S. Northeast states that participate in the Regional Greenhouse Gas Initiative (RGGI). Success? Yes — but also a signal that it’s time for stakeholders to consider the next step for RGGI. Jordan Stutt of the Acadia Center explains.

Declining Emissions Signal Need for Reform

In advance of expected actions by the Trump administration to remove or weaken federal climate protections, the Northeast’s pioneering climate program continues to see reductions in carbon pollution, reflected by today’s three-year low auction clearing price. Member states must now strengthen the Regional Greenhouse Gas Initiative to preserve the program’s effectiveness and signal commitment to continuing bi-partisan climate leadership.

Introduction

CO2 emissions from power plants have been steadily declining across the nine states of the Regional Greenhouse Gas Initiative (RGGI) for the last decade, and in 2016 fell 8.4 percent below the emissions cap. Since the program began in 2009, the decarbonization of the electric sector has been a major victory for the environment, health and economy of the region. Continued investments in clean energy and complementary climate policies in the participating states will help to achieve greater emissions reductions, but the RGGI states must do more to build on their first-in-the-nation program. Through the current Program Review,1 the participating states should strengthen RGGI to align the program with the current emissions trends and future climate goals.

Emissions

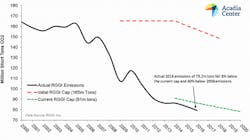

RGGI CO2 emissions fell to 79.2 million tons in 2016, a 4.7 percent decrease from 2015, marking the sixth consecutive year of power-sector emissions declines. Since 2008, the year before RGGI began, emissions are down 40.4 percent.

While several factors including growth in renewable energy, efficiency improvements, and fuel-switching have contributed to regional emissions reductions, a large share of these reductions has been attributed to the RGGI program.2 By establishing a price on carbon emissions and generating revenue for clean energy investments, RGGI has accelerated the transition to a cleaner electric sector. Increases in energy efficiency and growth in renewable energy output will enable the RGGI states to continue to achieve ambitious emissions reductions.

Figure 1: RGGI Emissions Continue to Fall

Market Dynamics

Auction Results

RGGI’s success has resulted in lower-than-expected emissions, which, in turn, have resulted in lower-than-projected compliance costs. With annual emissions falling below the RGGI cap in each of the program’s first eight years, there is an excess of allowances in circulation, leading to low allowance prices. Following ten consecutive auctions in which the auction clearing price was determined by the price floor—the lowest price at which allowances will be sold at a given auction—the RGGI states decided to reduce the cap by 45 percent. That decision had immediate impacts on the RGGI market, driving increased demand for allowances. Increased RGGI allowance prices proved to be temporary, however, as continued emissions reductions have outpaced the decline of the recently adjusted cap, creating an allowance oversupply. These conditions have resulted in falling allowance prices, with Auction 35 clearing at a three-year low of $3.00, 15 percent below the previous auction and 43 percent below the clearing price from one year ago.

Figure 2: Allowance Oversupply Leads to Low Auction PricesAllowance Oversupply

RGGI, like nearly all emissions trading programs, has struggled with an oversupplied market. Emissions reductions have been achieved more quickly and cost effectively than projected, creating a large gulf between cap levels and actual emissions, as shown in Figure 1. This has led to a market flooded with low-priced allowances, diminishing the program’s impact and undermining the environmental integrity of the cap. Recognizing these problems, the RGGI states agreed during the previous Program Review to gradually eliminate allowances banked prior to 2014 by adjusting 2014-2020 cap levels downward.3

This innovative strategy has proved effective, but a new surplus of allowances has been accumulated since 2014, and we expect it to increase through 2020 as trends that have contributed to the decline in emissions (growth in renewable energy, efficiency improvements, and fuel-switching) continue to bring emissions down.

In the first three years under the new cap, emissions have fallen below cap levels by 4.7 million tons (2014), 5.6 million tons (2015) and 7.3 million tons (2016). Over these three years all available allowances have been purchased, creating a surplus of 17.6 million tons. Additional allowances purchased from the Cost Containment Reserve (CCR) have added to the surplus, introducing 15 million additional allowances without corresponding emissions to balance the market. This brings the new surplus to 32.6 million tons, as shown in Figure 3. If emissions follow projections under recent ICF modeling of a post-2020 2.5% cap decline,4 the surplus will grow to 52.8 million tons through 2020. If CCR allowances are purchased, that figure could grow by up to 40 million tons.

Figure 3: Allowance Surplus, 2014-2020Need for Market Reform

The emissions reductions achieved by the RGGI states have been a tremendous success, but program reforms will be necessary to ensure that this success continues. As detailed in Part II of our RGGI Status Report: Achieving Climate Commitments,5 the RGGI states should make the following changes to strengthen the program:

- Establish a 2021-2030 cap that declines annually by 5% of the 2020 baseline;

- Commit to an adjustment for banked allowances accumulated from 2014-2020;

- Eliminate the CCR or increase CCR price triggers to ensure that CCR allowances are only purchased during periods of exceptionally high demand;

- Establish an Emissions Containment Reserve6 to capitalize on emissions reductions and to protect against future allowance oversupply; and

- Increase the auction reserve price to at least $4/ton to maintain a meaningful price on carbon emissions.

1For more information on the current RGGI Program Review, see: http://rggi.org/design/2016-program-review

2Why Have Greenhouse Emissions in RGGI States Declined? An Econometric Attribution to Economic, Energy Market, and Policy Factors, Brian Murray and Peter Maniloff, Duke Nicholas Institute, August 2015. Available at: https://nicholasinstitute.duke.edu/environment/publications/why-have-greenhouse-emissions-rggi-states-declined-econometric-attribution-economic

3This adjustment was conducted in two steps; one adjustment to account for allowances banked during the first control period (2009-2011) and a second adjustment for the second control period (2012-2014). For more information, see: https://www.rggi.org/docs/SCPIABA.pdf

4IPM modeling conducted by ICF for RGGI, Inc. available here: http://rggi.org/design/2016-program-review/rggi-meetings

5RGGI Status Report Part II: Achieving Climate Commitments, Acadia Center, August 2016. Available at: http://acadiacenter.org/wp-content/uploads/2016/08/Acadia-Center_RGGI-Report-2016_Part-II.pdf

6The Emissions Containment Reserve (ECR) was first proposed by the RGGI states during the November 21st, 2016 Stakeholder Webinar: http://rggi.org/docs/ProgramReview/2016/11-21-16/2016_Nov_21_ECR_Presentation.pdf. For more information on how the ECR might function, see: http://www.rff.org/events/event/2017-02/emissions-containment-reserve-rggi-how-might-it-work

Jordan Stutt is Policy Analyst in the Acadia Center’s Boston office.